Insider filing report for Changes in Beneficial Ownership

- Schedule 13G & 13D forms are used to report a party's ownership of stock which exceeds 5% of a company's total stock issue.

- Schedule 13G is a shorter version of Schedule 13D with fewer reporting requirements.

- Peter Lynch

What is insider trading>>

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| SCHEDULE 13D/A | |

|

Under the Securities Exchange Act of 1934 (Amendment No. 5)* | |

|

Absolute Software Corporation | |

| (Name of Issuer) | |

|

Common Shares, no par value per share | |

| (Title of Class of Securities) | |

|

00386B109 | |

| (CUSIP Number) | |

|

Jonathan Brolin Edenbrook Capital, LLC 116 Radio Circle Mount Kisco, NY 10549 (914) 239-3117

with a copy to:

Adriana Schwartz, Esq. Schulte Roth & Zabel LLP 919 Third Avenue New York, New York 10022 (212) 756-2000 | |

| (Name, Address and Telephone Number of Person | |

| Authorized to Receive Notices and Communications) | |

|

May 18, 2023 | |

| (Date of Event Which Requires Filing of This Statement) | |

If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of Rule 13d-1(e), Rule 13d-1(f) or Rule 13d-1(g), check the following box. [ ]

(Page 1 of 7 Pages)

______________________________

* The remainder of this cover page shall be filled out for a reporting person's initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page.

The information required on the remainder of this cover page shall not be deemed to be “filed” for the purpose of Section 18 of the Securities Exchange Act of 1934 (“Act”) or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however, see the Notes).

| CUSIP No. 00386B109 | SCHEDULE 13D/A | Page 2 of 7 Pages |

| 1 |

NAME OF REPORTING PERSON Edenbrook Capital, LLC | |||

| 2 | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) ¨ (b) ¨ | ||

| 3 | SEC USE ONLY | |||

| 4 |

SOURCE OF FUNDS AF | |||

| 5 | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT TO ITEMS 2(d) or 2(e) | ¨ | ||

| 6 |

CITIZENSHIP OR PLACE OF ORGANIZATION New York | |||

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON WITH: |

7 |

SOLE VOTING POWER -0- | ||

| 8 |

SHARED VOTING POWER 5,506,989 | |||

| 9 |

SOLE DISPOSITIVE POWER -0- | |||

| 10 |

SHARED DISPOSITIVE POWER 5,506,989 | |||

| 11 |

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON 5,506,989 | |||

| 12 | CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | ¨ | ||

| 13 |

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) 10.38% | |||

| 14 |

TYPE OF REPORTING PERSON IA, OO | |||

| CUSIP No. 00386B109 | SCHEDULE 13D/A | Page 3 of 7 Pages |

| 1 |

NAME OF REPORTING PERSON Jonathan Brolin | |||

| 2 | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) ¨ (b) ¨ | ||

| 3 | SEC USE ONLY | |||

| 4 |

SOURCE OF FUNDS AF | |||

| 5 | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT TO ITEMS 2(d) or 2(e) | ¨ | ||

| 6 |

CITIZENSHIP OR PLACE OF ORGANIZATION United States | |||

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON WITH: |

7 |

SOLE VOTING POWER -0- | ||

| 8 |

SHARED VOTING POWER 5,506,989 | |||

| 9 |

SOLE DISPOSITIVE POWER -0- | |||

| 10 |

SHARED DISPOSITIVE POWER 5,506,989 | |||

| 11 |

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON 5,506,989 | |||

| 12 | CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | ¨ | ||

| 13 |

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) 10.38% | |||

| 14 |

TYPE OF REPORTING PERSON IN | |||

| CUSIP No. 00386B109 | SCHEDULE 13D/A | Page 4 of 7 Pages |

This Amendment No. 5 (“Amendment No. 5”) amends and supplements the statement on Schedule 13D filed with the Securities and Exchange Commission (the “SEC”) on October 7, 2021, as subsequently amended on Schedule 13D (as amended thereby and hereby, the “Schedule 13D”), with respect to the Common Shares, no par value (the “Common Shares”), of Absolute Software Corporation (the “Issuer”). Capitalized terms used herein and not otherwise defined in this Amendment No. 5 have the meanings set forth in the Schedule 13D. This Amendment No. 5 amends Items 3, 4, 5(a)-(c) and 7 as set forth below.

| Item 3. | SOURCE AND AMOUNT OF FUNDS OR OTHER CONSIDERATIONS |

| Item 3 of the Schedule 13D is hereby amended and restated as follows: | |

| Shares reported represent 5,506,989 Common Shares of the Issuer. |

| The net investment costs (including commissions, if any) of the Common Shares directly owned by the private investment funds advised by Edenbrook is approximately $57,288,370. The Common Shares were purchased with the investment capital of the private investment funds advised by Edenbrook. |

| Item 4. | PURPOSE OF TRANSACTION |

| Item 4 of the Schedule 13D is hereby amended and supplemented as follows: | |

| As disclosed in the Reports of Foreign Private Issuer filed by the Issuer on May 11, 2023 and May 17, 2023, on May 11, 2023 the Issuer entered into an arrangement agreement pursuant to which affiliates of Crosspoint Capital Partners, L.P. have agreed to acquire all of the issued and outstanding Common Shares of the Issuer at a price of US$11.50 per Common Share (the “Acquisition”). On May 18, 2023, Edenbrook sent a letter (the “May 18 Letter”) to Dan Ryan, The Chairman of the Board, expressing Edenbrook’s strong belief that the terms of the Acquisition significantly undervalue the Issuer. The May 18 Letter details and provides support for Edenbrook’s belief that the Acquisition undervalues the Issuer. | |

| The foregoing summary of the May 18 Letter is not intended to be complete and is qualified in its entirety by reference to the full text of the May 18 Letter, which is filed herewith as Exhibit 2 and is incorporated herein by reference. | |

| Item 5. | INTEREST IN SECURITIES OF THE ISSUER |

| Items 5 (a)-(c) of the Schedule 13D is hereby amended and restated as follows: | |

| (a) | As of the date hereof, Edenbrook and Mr. Brolin may be deemed to be the beneficial owners of 5,506,989 Common Shares, constituting 10.38% of the outstanding Common Shares, based upon 53,059,224 Common Shares outstanding as of March 31, 2023, based on the information set forth in Exhibit 99.1 to the Report of Foreign Issuer on Form 6-K filed by the Issuer with the SEC on May 15, 2023. |

| (b) | Edenbrook and Mr. Brolin have the sole power to vote or direct the vote of 0 Common Shares; have the shared power to vote or direct the vote of 5,506,989 Common Shares; have the sole power to dispose or direct the disposition of 0 Common Shares; and have the shared power to dispose or direct the disposition of 5,506,989 Common Shares. |

| CUSIP No. 00386B109 | SCHEDULE 13D/A | Page 5 of 7 Pages |

| (c) | The transactions by the Reporting Persons in the Common Shares during the last sixty (60) days are set forth in Schedule A. All such transactions were carried out in open market transactions. |

| Item 7. | MATERIAL TO BE FILED AS EXHIBITS |

| Item 7 of the Schedule 13D is hereby amended and supplemented as follows: | |

| Exhibit 2 | May 18 Letter. |

| CUSIP No. 00386B109 | SCHEDULE 13D/A | Page 6 of 7 Pages |

SIGNATURES

After reasonable inquiry and to the best of his or its knowledge and belief, each of the undersigned certifies that the information set forth in this statement is true, complete and correct.

Date: May 18, 2023

| EDENBROOK CAPITAL, LLC | ||

| By: | /s/ Jonathan Brolin | |

| Name: | Jonathan Brolin | |

| Title: | Managing Member | |

| EDENBROOK LONG ONLY VALUE FUND, LP | ||

| By: Edenbrook Capital Partners, LLC, its General Partner | ||

| By: | /s/ Jonathan Brolin | |

| Name: | Jonathan Brolin | |

| Title: | Managing Member | |

| By: | /s/ Jonathan Brolin | |

| JONATHAN BROLIN |

| CUSIP No. 00386B109 | SCHEDULE 13D/A | Page 7 of 7 Pages |

Schedule A

TRANSACTIONS IN COMMON SHARES BY THE REPORTING PERSONS

The following table sets forth all transactions in the Common Shares effected by the Reporting Persons during the last sixty (60) days. Unless otherwise noted, all such transactions were effected in the open market through a broker.

| Trade Date | Shares Purchased (Sold) | Price Per Share ($) |

| 03/22/2023 | 10,000 | 7.5323 |

| 03/24/2023 | 2,562 | 7.5096 |

| 03/28/2023 | 25,000 | 7.4838 |

Exhibit 2

May 18, 2023

Dan Ryan

Chairman of the Board

Absolute Software Corporation

Suite 1400

Four Bentall Centre, 1055 Dunsmuir Street

Vancouver, British Columbia, Canada

V7X 1K8

Dear Dan:

Our firm, Edenbrook Capital, LLC, is a large shareholder of Absolute Software Corporation (“the Company” or “Absolute”), with ownership of approximately 10.38% of the company, based on the 53,059,224 shares outstanding in the Company’s 6-K filed on May 15, 2023. We have been patient, supportive shareholders for over five years, and in that time, we have enjoyed a collaborative, productive relationship with the Company. But following last week’s announcement of a proposed transaction for the Company to be taken private by Crosspoint Capital Partners (“Crosspoint”) at a price that significantly undervalues the Company (the "Proposed Acquisition"), we feel compelled to share our views publicly for the benefit of all shareholders. In short, we believe this transaction is unfair to public shareholders as it undervalues the Company and allows a prospective new owner to benefit from share price erosion caused by Company missteps, while public shareholders who supported the Company’s turnaround are left in the lurch.

Valuation, Part 1: Widening the Lens Makes the Price Premium Look Paltry, if not a Discount

In the May 11, 2023 press release announcing the Proposed Acquisition, Absolute CEO Christy Wyatt said that the deal would deliver “immediate cash value to our shareholders,” while the release also stated that the “cash consideration represents a premium of 34% and 38% to the closing price and 30-day volume-weighted average price, respectively, of the Common Shares on the Nasdaq on May 10, 2023.”

What the release fails to mention, however, is that the proposed $11.50 per share transaction represents only a $0.10, or 0.88% premium, to where the stock was trading when the Company’s fiscal second quarter results were announced the evening of February 14, 2023. Further, the proposed $11.50 per share price is a 3.85% discount to the 2023 closing high of $11.96 on February 2, and a 7.41% discount to the 52-week-high closing price of $12.42 on October 5, 2022. While we believe that the sell-off in the stock’s price that occurred after that February earnings call was an overreaction, given the strong fundamentals of the Company (which were further reinforced with the release of fiscal third quarter earnings after market close on May 15, 2023), we also believe that it was a combination of poor communication by management and poor balance sheet decisions by the Company that have caused Absolute to trade at such a sharp discount to public peers. As we’ll discuss later, we believe the Company slipped on a banana peel that they are responsible for dropping, paving the way for Crosspoint to harvest the fruits of success that public shareholders planted. How heartbreaking for public shareholders that the market’s reaction to the Valentine’s Day earnings report and call, during which management stressed the strength of the underlying business, caused the Company to lose its nerve and sell in a panic.

Valuation, Part 2: Deal Price is Not Even in the Ballpark on Private Market Value

While the February 14 earnings report did include a modest reduction in overall revenue guidance for the current Fiscal Year, the increased profitability guidance in that same report should actually yield a higher level of total profitability for the fiscal year ending June 30, 2023 than was originally guided to in the Company’s fiscal fourth quarter earnings report on August 23, 2022. More significantly, the Company’s Annual Recurring Revenue (“ARR”) highlighted in that February report continued to show real strength, growing once again in the mid-teens on a percentage basis (and by a record dollar amount on a sequential basis), with management projecting continued similar strength for the remainder of the fiscal year. We think ARR is a far more critical metric than reported accounting revenue, as ARR shows the company’s actual, ongoing book of business, and gives a clearer picture of management’s ability to grow the business, while reported accounting revenue can be optically impacted by changing deal lengths and other factors. But don’t just take our word for it: on that same earnings call, management repeatedly stressed the importance of ARR, as opposed to focusing on overall revenue, with CFO Jim Lejeal stating, “we're notably focusing on ARR as the right reflection of the growth of the business.”

We were glad to hear management’s additional emphasis on the importance of ARR on that earnings call because ARR is also the key metric used in valuations for acquisitions in the cybersecurity software space. And on that score, how did the Company perform in securing value for its public shareholders under the terms of the Proposed Acquisition? An Absolute Failure.

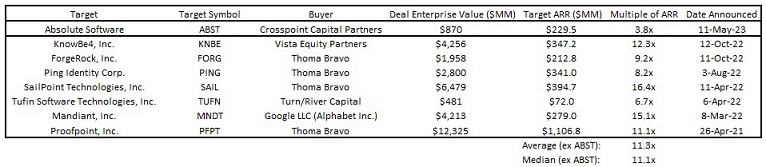

The table below shows cybersecurity software acquisitions that have occurred since the second quarter of 2021, which we believe is the relevant time period because that is when the Company itself announced its acquisition of secure access provider NetMotion. As the table shows, multiples of ARR for these transactions ranged from 6.7x to 16.4x, with the average being 11.3x and the median being 11.1x. Based on the proposed $870 million enterprise value of Absolute in the Proposed Acquisition announcement, and the $229.5 million in ARR reported in the May 15, 2023 fiscal third quarter earnings report, the Board of Directors (“the Board”) has thus agreed to sell the Company for 3.8x ARR,

| 2 |

approximately one-third the average multiple in the table of comparable transactions. The deal with the lowest valuation multiple in the table was for Tufin Software, which had nearly identical revenue growth to Absolute at the time of its deal announcement. But while Absolute has adjusted EBITDA margins north of 25%, Tufin had margins in the negative teens. In other words, a similarly growing company with EBITDA margins nearly 4000 basis points lower sold for approximately three additional multiple turns as compared to the ARR valuation that the Proposed Acquisition represents.

Source: FactSet, Bloomberg and company filings; PFPT reports Billings; ARR shown from the full quarter ended prior to deal announcement date

If you were to put the Tufn 6.7x multiple on Absolute’s ARR, you would get an enterprise value of approximately $1.538 billion. Subtracting the Company’s net debt of approximately $213 million would yield an equity value of approximately $1.325 billion, and with 53.1 million shares outstanding, a per share equity value of approximately $24.97 per share, more than double the Proposed Acquisition price of $11.50 per share. Even the lower 6.2x ARR multiple that Absolute paid for NetMotion would yield an equity value of approximately $22.80, nearly double the Proposed Acquisition price.

As the Company has taken pains to discuss publicly many times over the last few years, Absolute has significant strategic value because of its undeletable presence in the firmware of over half a billion devices, its ability to use that presence to protect other software that sits on the application layer through its Persistence offering, and increasing industry needs for solutions that solve both secure endpoint and secure access needs in an integrated fashion, which Absolute does. Because of its relatively under-sized enterprise salesforce for the industry, we believe Absolute is much smaller than it could be: were a larger strategic player with a globally distributed sales force to acquire the Company, it could reach a much wider audience more quickly. Out of more than 600 million devices it is embedded on, Absolute is activated on approximately 14 million, or just over 2%. That gives the company, on its own or with a partner, an enormous amount of runway to grow, and the secular forces in the industry are increasing the need for its offerings.

So why is the Board selling to a private equity firm, instead of to a strategic acquiror who could better distribute the Company’s offerings? And why is the Board selling at such a discount to private market transactions, especially when recent third quarter earnings showed that the second quarter earnings report was not symptomatic of a larger fundamental issue? We look forward to reviewing the pending filing of the Circular that will show the deal process that transpired. Did the Board really maximize value by shopping the Company during a quarter that included a near collapse of the regional banking system? Is that the best time to get the attention of prospective buyers?

| 3 |

Valuation, Part 3: A Standalone Absolute is Worth Much More than the Proposed Acquisition Price

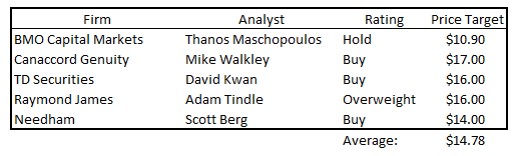

As a standalone business before the announcement, Absolute was trading at an approximately 60% discount to comparable security software companies. Further, according to FactSet, here were the 2023 target prices for Absolute, based on sell-side firm estimates, as of May 10, the day before the Proposed Acquisition was announced:

That’s an average price target for this year of $14.78, which is 28.5% above the Proposed Acquisition price. In other words, based on sell-side estimates, public shareholders could have achieved a nearly 30% improvement over the Proposed Acquisition price as a standalone company this year. Where’s that immediate cash value public shareholders were promised in the press release? And that $14.78 is just a trading estimate. Using the same 38% premium to trading price that the Company cited in the May 11 press release, and applying it to the average price target, would yield a per share value of $20.40, nearly $10, or 77% above the Proposed Acquisition price.

What We’ve Got Here is Failure to Communicate

While we believe that Christy Wyatt has built a business of extraordinary strategic value, we also believe that numerous unforced errors related to financial communications have held the stock back and created this situation in which Crosspoint could swoop in during a moment of perceived weakness to try to take the Company for a song. War and Peace would be a shorter read than a full list of investor relations missteps, but here are some of the more egregious examples that have been costly to public shareholders:

| 1) | On the May 11, 2021 earnings call, the Company discussed the acquisition of NetMotion, announced that same day. Former Absolute CFO Steven Gatoff said on that earnings call: “we expect the acquisition to be accretive on a forward-looking basis to ARR growth, revenue growth and adjusted EBITDA margin.” The market cheered this news, sending the stock to $15.25, a level it has never seen again. However, when the Company provided Fiscal Year 2022 guidance on August 10, 2011, which was after the NetMotion deal had closed in July, the Company guided for a slowing of revenue growth and lower adjusted EBITDA margins. That is not what “accretive on a forward-looking basis” means, and the stock sold off meaningfully, the first of three consecutive quarters in which there was a stock sell-off caused by a disconnect between what the CFO said and what was produced in an earnings report. |

| 4 |

| 2) | To finance the NetMotion acquisition, the Company took on floating-rate debt at the bottom of a historically low, Federal Reserve-suppressed, interest rate environment, which had only one way to go: up. We believe fixed rate debt at the time could have been secured for closer to 6%, but instead, the Company stuck with floating rate debt, refused to hedge the debt at all, and is currently paying rates north of 11%, an unnecessary, and completely avoidable, tax on cash generation. What kind of oversight did the Board provide here? |

| 3) | Also at the time of the acquisition, then-CFO Gatoff claimed that the company would rapidly de-lever, from over four times EBITDA at the time of the acquisition, to under two times within two years. With one quarter left on that clock, the Company is still approximately four times levered. While the core business has generated, and continues to generate, cash to comfortably service this debt load, in our opinion it was an unnecessarily bold statement by the Company, and it was not rooted in mathematical reality. We believe that statements such as these eroded shareholder confidence in management and weighed on the stock. |

| 4) | After Mr. Gatoff left the Company in March 2022, he was replaced on an interim basis by Ron Fior, who we thought was excellent. One need only see Mr. Fior’s presentation at the Company’s Investor Day in September 2022 to see how clearly and accurately he spoke about the Company’s financials. Unfortunately, Mr. Fior did not stay on as the full-time CFO, and between his appointment and that of his replacement in late 2022, no progress was made on refinancing the debt, with its ever-increasing interest rate. |

| 5) | Mr. Fior was replaced by Jim Lejeal, who started as CFO in December 2022. Mr. Lejeal was on one earnings call, the Valentine’s Day Massacre. We think it was a major mistake not to have Mr. Fior stay on to bridge that call, as Mr. Lejeal had only been CFO for a short while, and did not know the Company well enough at that point to answer investor questions clearly, which turned minor issues of contract length and a modest revenue guidance cut into a referendum on the Company’s balance sheet. This was a major financial communications/investor relations snafu, and it was completely avoidable. Is anyone on the Board thinking about the impact of these kinds of decisions on shareholders? |

Deliver Absolute Value for Shareholders

Persistence and Resilience are the names of two of Absolute’s core product offerings. It would have been nice if the Board had shown more of both in order to maximize shareholder value. Perhaps another enterprising buyer, realizing how cheaply the Board is willing to sell the Company, will come along and bid a higher price. Shame on you if you don’t let them.

| Sincerely, | |

| Jonathan Brolin | |

| Founder and Managing Partner |

| 5 |